Excalibur. (Any views expressed in the below are… | by Arthur Hayes | Jul, 2022

(Any views expressed in the below are the personal views of the author and should not form the basis for making investment decisions, nor be construed as a recommendation or advice to engage in investment transactions.)

(Note to reader: this week’s essay is a continuation of my piece from last week, “A Samurai, a Knight, and a Yankee”. I recommend reading that entry first before diving into this one.)

What an evening. I retired to the shed out back to sleep. It took me much longer than usual to doze off, as I gleefully replayed the night’s conversation over and over again in my head. But after several hours, sleep finally came. And then…

Clickity-clack. Clickity-clack. The hoofs of a fast horse thundered down the Road to Hyperinflation. I sat up. Who could that be at this hour? I stumbled out onto the porch of the inn. Lo and behold, it was a messenger.

“Announce yourself!” I bellowed.

“Be not afraid, innkeeper — I am just a messenger, sent from far yonder on the eastern front. I have an urgent message for Lady Lagarde.” He waved an imperial sealed envelope in front of me.

I ran to the stable where Lady Lagarde was sleeping and shook her awake. “Lady, there is a squire here with an urgent message for you. Please come out front.”

She was clearly displeased that her slumber had been disturbed, grumbling softly to herself as she rose from her bed. A few minutes later she presented herself, collected the envelope from the messenger, and tore it open.

‘Lady Lagarde, I hope this message finds you well. I am sorry to report that the Great Bear has been provoked into taking another extreme measure. The Bear has shut off the gas to a German fiefdom. They are looking to you for guidance — what shall they do? They depend so heavily on the Bear to power their formidable war…I mean, ahh, manufacturing economy, which they need to continue powering the Kingdom of the Euro. And even worse, the summer sun has burned brighter these last few years. The people are hot, but cannot cool themselves due to a lack of energy. They are managing for now, but winter is fast approaching. The heat is uncomfortable, but the cold will be deadly. In only a few months, many of our nobles must provide heat for their subjects. Where oh where will this heat come from without the Bear? Damn it to Dante’s 9th Circle of Hell.

And that’s not all — while you have been out enjoying your bucolic summer ride with Sir Powell and Kuroda-dono, the Euro has dropped substantially in value and is now equal to the Dollar. Oh, the horror! What are we to do, Lady Lagarde? How will we power our economy, heat the homes of the common folk, and print the Euro to buy the loyalty of our nobles?

– Sergio, Your Humble, Well-Paid Servant, ECB

Lady Lagarde looked up from the note. “Innkeeper, fetch me a pen and some parchment,” she snapped. “I must respond to Sergio quickly to avert this crisis.”

I shuffled silently behind the front desk of the inn, pulled out the utensils she had requested, and returned to her.

Pen in hand, she wrote the following:

‘Sergio–

Thank you for your haste in delivering this sobering message. The Great Bear shall not succeed. The Bear does not know that I have secured the support of Sir Powell. He has pledged to print the Dollar and buy our Euro bonds — boosting the value of our currency against theirs so that we can afford to pay his kingdom for its energy instead. I know not how long it will take to ship these commodities across the Atlantic, or whether this would be faster than resuming normal diplomatic relationships with the Bear and receiving their commodities by pipeline. But it shall be done.

I must caution, though, that Sir Powell still needs the support of his royal Grandmother, Dowager Empress Yellen. Only she can give the order, but he assures me she will do her duty. Take this message, Sergio, and spread the word — I, Lady Lagarde — like Joan of Arc before me — will not fail the kingdom of the Euro.

P.S. I recently acquired the power of the alphabet. I alone can put together letters and conjure freshly printed Euros out of thin air. Remember these letters — T … P … I.

– Lady Lagarde, Better-Paid Servant, Bosslady of the ECB

Lady Lagarde finished scribbling and signed her note with a dramatic flourish. She folded the parchment and handed it to Sergio’s messenger. “Move with haste to deliver my message. And tell Sergio to fear not, for I shall be done with my holiday early. I recognise the gravity of this bastardly Bear’s deeds, and so I shall rest for just seven weeks rather than my usual eight before returning to the front to fight.”

The question of how to govern — and in particular, the degree to which it is done federally vs. locally — is one that plagues every large country. There is no governing philosophy that, scaled to a certain size, doesn’t require some degree of decentralisation. But decentralising the government also raises tricky questions around how to tax and allocate resources between the federal and local vestiges of the government.

The EU is doomed to fail because it is solely a monetary union, and it does not have federal powers to collect taxes and force economic harmony between its country members. Because every country in the EU pursues different policies, each one faces different economic outcomes. Some are more prosperous than others, and there’s no way for the centre to move resources between its member states. But at the same time, all states share the same currency and monetary policy — which is not always suitable for their specific economic circumstances.

As a result, some countries are perceived as safer or more worthwhile sovereign credit risks than others. The member states can issue their own Euro-denominated country bonds but cannot print Euros. Therefore, these bonds are not risk-free in Euro terms. They would only be risk-free if the European Central Bank (ECB) fully commits to printing Euros to pay back member states’ government debts in any and all circumstances. The ECB could have been set up with such a proviso; however, the ECB’s sole legal mandate is stabilising the general price level of the EU, and that’s it. All other policies are subordinated to that mandate.

The problem is that, when faced with inflation, the ECB’s mandate technically requires it to tighten monetary policy to keep prices down. This means that if a country cannot afford its national debt load during an inflationary period, the ECB cannot legally ride to the rescue and print Euros when doing so would push up the general price level.

But what the law prescribes as the ECB’s mandate and what the ECB views as its mandate are two different things. The ECB is really only concerned about maintaining the EU as a monetary and political entity — even if that means eschewing its legal mandate and stoking the fires of inflation. Leaving a member state to struggle helplessly under its Euro-denominated debt load can drive that member state to leave the Euro and redenominate all of its debts in a new national currency, which its central bank can print freely (much to the chagrin of its investors, who then get paid back in the weaker new national currency, rather than the Euro). This is called a technical default. (If you want to understand how this works in practice, study the last two centuries of Argentinian monetary policy.) An EU member entering technical default and leaving the EU to resolve its debt problems is the ECB’s worst nightmare — and it will do pretty much anything in its power to prevent that outcome.

The structural problems of the EU monetary union came into focus in a big way from 2009–2011, when a number of European countries struggled to pay off the massive debts they had accrued over the preceding decades. Here is a good article describing the crisis. Super Mario Draghi, head of the ECB, responded by proclaiming that he would “do whatever it [took]” to ensure no country left the Euro. The ECB then printed billions of fresh Euros and started using them to purchase the bonds of its weakest members.

But the market heard Draghi’s proclamation and did the correct thing, which was to front-run the ECB’s purchases. Investors bought up the cheap bonds they knew the ECB would predictably buy month after month at a cheap price, and then sold them back to the ECB at a more expensive rate. The bond yields of the sickly EU members plummeted, and the problem was kicked down the road until 2022.

The EU is a sprawling bureaucracy made up of a few nationally elected members, and a lot of other apparatchiks that draft and implement policy. In 2022, the EU plans to spend EUR 1.13 billion on staffing-related costs (salaries, travel, residences etc.). There are approximately 8,000 people working in the EU bureaucratic machine. That equates to an average annual salary of EUR 142,000. Not bad! Compare that with the average EU dual income family of 4 at approximately EUR 55,000, and you’ll start to understand why EU bureaucrats want to keep the game going as long as possible. Without the EU, there would be no ECB, and no phat paychecks.

The goal of the human species is to survive and procreate. It follows, then, that an organisation of humans has the same goals. The ECB will always do whatever it takes to ensure the EU is still a thing. If pesky things like EU inflation hitting 30-to-40-year highs get in the way, they can be explained away as “transitory”, thereby allowing the ECB to avoid its legal obligation to tighten monetary policy. The ECB can instead continue printing money, keeping countries from leaving the Euro due to their unaffordable government bond yields.

The issue that the ECB faces today is that investors are starting to question if the ECB will continue to “do whatever it takes” to keep the union together. For now, it is — the ECB still maintains a negative policy rate — but inflation has begun to hit levels that may become very difficult to write off as “transitory” moving forward.

Every culture has fables and allegorical stories told to children about old miserly individuals with too much money and not enough compassion for their fellow humans. Scrooge McDuck of Ducktales is my personal favourite. Ol’ Scrooge loved to hoard his money (especially gold — brah, I’m with you on that!) and he obviously grew his stash with fine investment acumen and an ability to delay gratification. Let’s put ourselves in his shoes and imagine that his private wealth manager — we’ll call her Goldy Rothschild — paid him a visit with an investment he just HAD to look at.

Goldy showed up to the meeting with a Kelly bag full of prospectuses for a variety of Euro-area government bonds, which she said were all at once-in-a-lifetime levels.

As Mr. McDuck, you are rightfully suspicious any time your banker calls you with the “deal of the century.” Usually, whatever trade or investment idea Goldy is pitching is a sign you should do the exact opposite.

You know that if a bond’s yield is to be worthwhile, it needs to cover both the rate of inflation and the credit risk of the borrower. So, you ask Goldy a few questions.

“Goldy, can you tell me the most recent inflation readings for the Euro area?”

“Of course — the most recent year-on-year EU inflation (HICP) reading came in at 8.6%” she responds.

“Wow, Goldy — inflation is running quite hot,” you say, eyes darting over the chart in front of you. “I should hope that, at a minimum, the bond yields have risen to cover the rate of inflation. Can you tell me the most recent weighted average yield on EU 10-year bonds?”

Goldy’s shit is tight, and she quickly calculates the 10-year yield where each member state’s current 10-year yield or closest equivalent maturity bond is divided by total EU debt outstanding. “It’s 2.20%.”

Wowzers — these bond yields are not even close to covering the cost of inflation. And even worse, if these countries leave the Euro, then the debts would most likely get redenominated into a weaker national currency. To say these yields don’t compensate for that risk would be a gross understatement.

“Goldy, these yields are paltry. Do you know what percentage of annual EU GDP the interest payments would represent if, on average, every state borrowed at the 8.6% inflation rate?”

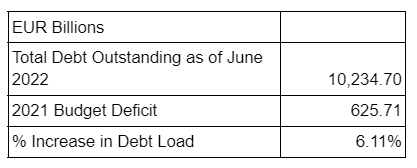

“One second, sir.” Goldy quickly steps into the waiting room, where her analyst Macron Macaroon is sitting. She instructs him to prepare the analysis. You smirk to yourself, as you spot Macron is sporting the latest gilet jaune get-up designed by Margiela. Macron is quite the adroit banker, and within ten minutes sends over the analysis to Goldy. He went onto Eurostat, downloaded the total debt outstanding as of June 2022, and calculated the interest payment amount. It came out to 7.17% of GDP per year.

“Goldy, these numbers are terrible!” You remark, eyes wide with concern. “I hope that EU countries are at least running budget surpluses, so that their debt load will decrease over time. Is that the case?”

“I’m sorry, Mr. McDuck — that is not the case. Every single member runs a deficit except for Luxembourg, and they don’t actually need any help, to be honest. I should also add that, due to a slow recovery from the COVID pandemic and less economic activity due to increased energy costs, their balance sheets will get worse before they get better. So that I’m being completely forthright about the current state of affairs, take a look at the below table I put together.”

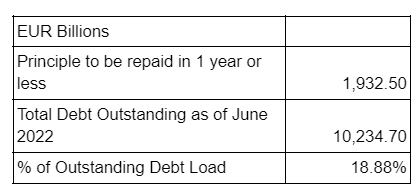

You shake your head and continue. “So the debt load will increase by over 6% just to fund 2022 expenditures– how much debt will need to be issued just to repay the principle of maturing debt?”

She shares another table with you.

“Goldy, Goldy, Goldy… now I know why they sent you scrambling around the world to find suckers to buy these bonds. The EU needs to find buyers for a gargantuan amount of bonds IMMEDIATELY. But maybe there is some silver lining to these stats. Does the EU at least run a trade surplus with the rest of the world that would cause some entity to have to recycle Euros back into EU government bonds?”

Goldy slowly shakes her head, indicating that is not the case. “The trade balance has deteriorated rapidly this year. The most recent figure for May 2022 came in at close to a EUR 82 billion deficit — meaning the EU owes the world money, and not the other way around. Take a look at this depressing chart depicting the degradation of the EU macroeconomic fundamentals.”

“Goldy, you brought me a similar list of shitty government bonds in 2011.” (And actually, you think to yourself, the 2011 situation was probably a bit better than today. At least the EU wasn’t being sacrificed by America to host the front line in a proxy war with Russia.) “But you assured me the ECB would buy everything in the future at higher prices than what I paid for them. Can you offer me a similar guarantee today?”

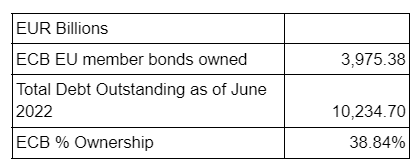

“Before I go into the nitty gritty of whether or not the ECB can buy these bonds, I should tell you that the ECB already owns almost 40% of all EU member state bonds outstanding.”

Goldy squirmed a bit. “Unfortunately, it is unclear whether the ECB can legally purchase more of these bonds, given that inflation in the EU is running at 30-to-40-year highs. They came out with this half-assed proposal to reduce what they call ‘Fragmentation Risk’, which is a fancy way of saying they will buy the weaker members’ bonds so that the yields converge with those of the stronger members. But if all the yields rise in parallel, they haven’t explained how they would deal with that outcome. In short, I am not confident — particularly given the recent statements made by Christine Lagarde — whether they fully stand behind their promise to ‘do whatever it takes’ to prevent the weakest members from abandoning the Euro currency to fix their own government finances.”

This is truly a FUBAR situation. You summarise in your head all the terrible metrics you just heard. The current yields don’t compensate for inflation and redenomination risk. The amount of debt issuance is set to increase dramatically, both to fund large and increasing government deficits and to repay old debt. Even worse, the EU as a trade bloc now owes the world money, rather than the other way around. And to top it all off, the ECB, who is essentially the buyer of last resort and owns 40% of the market, might have to step away for a bit due to inflation at 30-to-40 year highs. And they want me to buy these bonds– LOLZ.

“Thank you for your honesty, Goldy. I think I’ll pass on these bonds for now. But please do let me know when the ECB commits to printing Euros to buy bonds in an amount sufficient to fund the increasing budget deficits of all the EU member states.”

Goldy nods her head, stands up, and begins quietly gathering her things.

“Brrring! Brrring!” Goldy’s phone buzzed and beeped furiously. “Wait, wait, Mr. McDuck — I just got a message that the ECB concocted a new alphabet soup program aimed at printing more money to support the weakest member states. It’s called the Transmission Protection Instrument (TPI). Basically, it gives the ECB the sole discretion to determine whether the market value of a member state’s bonds is unwarranted given certain macroeconomic fundamentals. If such a situation occurs, then the ECB is empowered to purchase any member state’s bonds in an unlimited amount.”

“So Goldy– this means that the ECB, at its sole discretion, gets to determine whether a situation requires more printed money?”

“Yes, Mr. McDuck. Exactly. The ECB just granted itself more powers.”

“Wow! That’s great. But I will still wait for them to be tested and actually start buying bonds. I am still uncertain whether they will be prepared to fully deploy the money printing bazooka if the Euro continues to weaken as a result of more currency printing. The ECB needs the Fed to lend a helping hand. So, I’m going to stay on the sidelines for this one.”

Goldy’s face dropped. Sensing her disappointment, I quickly offered up a consolation prize. “I don’t want you to leave empty handed, though — can I buy some Bitcoin through your bank?”

Goldy lets out a frustrated sigh. “You know, I have been travelling all around the world pitching these bonds to my clients. And at the end of my presentation, every single one asks me the same question. I’ll be honest with you once more. Unfortunately, selling you physical Bitcoin — or even gold, for that matter — doesn’t make my bank much money. They would much rather I sell you some paper derivative manufactured by my structurers that earns management fees for the bank every year. But obviously, if you purchase this type of product, you don’t actually own the underlying crypto or precious metal. In light of that, I simply don’t have a product that suitably protects your assets from inflation at the price you’re looking for.”

I hope this little tale illustrates the dilemma facing the ECB. Explicit Yield Curve Control (YCC) — whereby the ECB targets a general absolute level of government bond yields and then purchases member state bonds to achieve that target — is the only way it can coax investors into taking the inflation and redenomination risk associated with buying the weaker member states’ bonds. Anything short of YCC, and investors will shun those bonds. The EU member states will quickly find there is no one left to purchase the bonds they have issued to pay for their high and rising budget deficits. But printing more Euros (which is necessary for the EU to buy their member countries’ bonds and successfully implement YCC) will cause the exchange rate to fall, and energy costs — and most importantly, the cost of natural gas — will rise.

Without ECB support, EU governments will be unable to finance themselves affordably. Then the bankrupt governments must either enact crushing austerity measures, such as raising taxes and cutting healthcare spending, or leave the Euro and redenominate all their debt into new national currencies which they can print. And if they decide to do the latter, the ECB and most of the large Too-Big-To-Fail European banks will become insolvent, as they owe Euros to their depositors, but their debt assets will be redenominated into weaker currencies.

The unfortunate reality is that European countries must import a substantial portion of their energy needs, and the countries selling it to them won’t be interested in a newly created Euro-trash currency. Trading partners will demand “hard” currency, and when a nation runs out of EUR, USD, or gold, no one will trade with them. The Sri Lankan tragedy is case and point. Without affordable energy, any modern society will quickly collapse. That, ladies and germs, is how the next European kinetic conflagration begins. For if newly destitute European nations cannot trade using their domestic currency, they will try to force others to trade with them using their military.

Data Sources: Bloomberg, Eurostat, ECB

America’s stalwart allies, Japan and the EU, need help implementing YCC. They can’t afford to print the money necessary to buy back their own domestic bonds, so they need America’s support. But how could this work in practice?

The Fed is laser-eye-focused on subduing inflation. The most recent CPI print was another stinger, and the Fed must continue to tighten domestic monetary conditions. They will likely do this by raising the policy rate and reducing the size of their balance sheet by selling US Treasuries and Mortgage-Backed Securities (MBS).

As mentioned in Part 1 of this piece, the Fed’s policy is extremely aggressive compared to the monetary policy of Japan and the EU. When a country (or group of countries) engages in YCC, it must print money and buy back its own bonds in order to cap yields below the observed rate of inflation. Therefore, the BOJ and the ECB cannot run an aggressive monetary tightening program like the Fed. Interest rate parity thus dictates that the Yen and the Euro must depreciate vs. the Dollar due to the divergence in monetary policies.

The Fed can do one of two things to weaken the dollar so that its allies can continue to afford to import the goods they need while also engaging in YCC:

- Buy JGBs and EU member state bonds by printing dollars.

- Stop reducing the size of its balance sheet and cut its policy rate.

Of the two options, I believe the first is politically an easier sell than the second. This comes down to accounting. Let’s dig in.

The following is a direct quote from a report written in March 2021 from Office of Inspector General, Department of Treasury, which describes what the Exchange Stabilisation Fund (ESF) is authorised to do.

The Gold Reserve Act of 1934 established a fund to be operated by the Secretary of the Treasury (the Secretary), with the approval of the U.S. President. Section 10 of the Act provided that “For the purpose of stabilizing the exchange value of the dollar, the Secretary, with the approval of the President, directly or through such agencies as he may designate, is authorized, for the account of the fund established in this section, to deal in gold and foreign exchange and such other instruments of credit and securities as he may deem necessary to carry out the purpose of this section.”

Let’s walk through the order of operations:

- Treasury Secretary Janet Yellen decides that America, to help its allies, should weaken the Dollar by purchasing foreign government bonds. In this case, the Treasury should purchase Japanese Government Bonds (JGBs) and EU member state bonds.

- The Treasury instructs the Federal Reserve Bank of New York to execute this policy.

- Through its network of primary dealers, the NY Fed credits the Fed balances of a bank with USD in sufficient size to first sell USD and purchase JPY or EUR, and then use those Yen or Euros to purchase EU or Japanese bonds.

- The dealer then deposits those bonds into the ESF, which is a line item on the balance sheet of the NY Fed.

Under this plan, the aggregate Fed balance sheet rises — but the portion of the balance sheet that is targeted for reduction under the bank’s Quantitative Tightening (QT) program remains unchanged. This is extremely important.

The Fed telegraphed to the world — and most importantly, to the American public — that it is tightening domestic credit conditions by allowing its hoard of US Treasury and MBS to decline. This raises the effective borrowing rate for all financial assets for American individuals and businesses. They hope this will reduce borrowing demand, as America’s economy will contract if less credit is supplied to it — cooling inflation in the process.

A rise in the size of the ESF and a fall in the size of the holdings of Treasuries and MBS securities can happen concurrently. Therefore, the Fed can supply the dollars its allies require, and reduce domestic inflation. At least, in theory.

The big question is how many JGBs and EU bonds the Fed would have to purchase to relieve the pressure on the BOJ and ECB, respectively. Would a simple statement from Treasury Secretary Yellen declaring that her department has authorised the NY Fed to pursue such a strategy be enough for the market? At that point, would participants front-run future Fed purchases by gobbling up JGBs and EU bonds, doing the government’s work for it and lowering yields in the process? Or would the market want to see the Fed actually purchase billions of dollars of these bonds before being converted into full believers?

The Don of the Dollar still has credibility, in large part due to the perceived aggressiveness of his efforts to fight the current bout of domestic inflation. Therefore, I suspect that, at first, the market won’t actually care if the ESF balance rises or not. The simple announcement of America’s plan to systematically weaken the dollar will cause JGB and EU bond yields to plummet, as investors snap them up left and right in anticipation of a Fed buying spree. But given how fast things move these days, that reprieve will not last long. The entire world of financial analysts will be intensely focused on the month-to-month changes of the ESF balance, and at some point, someone is going to call the Fed’s bluff. JGB and EU bond yields will creep back up, and the Treasury (via the NY Fed) will actually have to start buying bonds.

Capital goes to where it’s best treated. If investors can sell negative real-yielding bonds to a buyer who must buy for political rather than economic reasons, then they will do so. Then, those investors will turn around and use their capital to buy risky assets like stocks, commodities, real estate, crypto, etc. This is where the magic begins. Inflation, at least as measured by the flawed CPI metric, will most likely peak by the November midterm elections — and at that point, the Fed can claim victory.

I remind readers that the only thing that will have really peaked is the rate at which prices were increasing, not the prices themselves. Don’t expect prices to actually decline and become more affordable to those whose incomes do not rise as quickly as food and fuel prices.

With inflation allegedly in the rear-view, the first port of call for these cash-flush investors will be developed market (read, American) big-cap tech stocks. These are the companies that benefit the most from a lower discount rate. As the stock market rises, the wealth effect on the 10% of the American population that owns 89% of all financial assets will cause a rebound in economic activity.

If we look at the political checklist of the US Treasury, this policy checks all the boxes:

- Allow America’s allies to continue pursuing YCC and retain a strong currency against the dollar, which lessens fuel import inflation. This reduces their desire to break ranks and purchase cheap Russian energy.

- Continue to tighten domestic financial conditions by selling Treasuries and MBS. Since the rate of change of price rises will have peaked, a victory can be claimed using a somewhat dishonest measure of inflation.

- This creates a market dynamic which causes the stock market (i.e., S&P 500 / Nasdaq 100) to rise and make rich people happy. This should stall the recession that started earlier in the year.

But what’s the cost?

When a central bank commits to YCC, its balance sheet grows slowly, then accelerates upwards in a nearly straight line — blowing through all previous asset-holding highs extremely quickly. Hyperinflation is non-linear, and the ESF balance will grow rapidly as everyone dumps their JGB’s and EU bonds into the Fed, and the Japanese and EU governments continue to issue bonds at an increasing rate to fund their budget deficits. Thankfully, this dynamic probably won’t be dramatically apparent until 2023, when the market really tests whether the Treasury will purchase ALL the bonds necessary to cap yields. What’s special about 2023 is that it’s a non-election year. And therefore, inflation is not going to be a problem the administration cares about — that is, until it becomes a PRESIDENTIAL election year in 2024. That is going to be a humdinger of a policy conundrum.

Let’s quickly backtrack to the second policy option I listed earlier (i.e., the Fed cutting its policy rate and pausing QT). This achieves an effect similar to the US buying the EU’s and Japan’s bonds, because it reduces the divergence in monetary policy between the Fed and the BOJ/ECB (thereby weakening the dollar against the Yen and Euro). However, this is a much a tougher sell politically, because if the Fed calls it quits on QT, it can only do so without raising alarm bells amongst the American public if it can credibly claim that either a) it has defeated inflation, or b) the recession it engineered is so painful it must ride to the rescue.

The backwards-looking economic metrics needed to politically justify a pivot will take time. That is time that Japan and the EU don’t have. When it starts getting cold in October, energy use will rise. If the JPY and EUR are trading markedly weaker vs. the USD and there is no arrangement to change the relative valuations of these currencies, then Japan and the EU will be extremely tempted to re-engage with Russia. Russia always has the most leverage in the winter. Whether it’s against generals who thought it was a good idea to fight a land war against Russia, or modern-day politicians who must provide affordable heating fuel for their plebes, when it gets cold, Russia possesses its greatest leverage.

And as I keep mentioning, it is an American election year. The Fed’s domestic monetary policy is pretty set in stone from now until mid-November, when the government can end the theatrical performance it has been putting on to curry votes. Therefore, I believe that if the Treasury and the Fed are to do anything to assist the kingdom of the Yen and the Euro in their existential fight against the Great Bear, printing USD and purchasing JGBs and EU bonds is the only politically- and time-efficient option.

I know y’all been waiting for this section. Thank you for indulging me by hopefully reading and digesting those many highfalutin’ words I be writin’.

What we as crypto degen traders really care about is the $USD liquidity conditions’ rate of change. The Fed is concerned about the PRICE of money (aka USD interest rates). We are concerned about the QUANTITY of money. And hopefully (assuming that you didn’t just skim the top of this piece and skip to this section) I’ve convinced you that the rate of change in the quantity of USD is likely to begin increasing shortly.

If the Fed starts increasing the size of the ESF, the quantity of USD sloshing around the world will increase and drive this metric higher. Crypto responds positively to an increase in the quantity of USD. The quantity of Bitcoin is fixed, therefore when the USD denominator grows Bitcoin’s relative value increases. Even before the Fed buys its first foreign bond, just the expectation of an increase in the quantity of dollars will spur prices of cryptos and various other risky assets higher.

Even though this current episode of USD liquidity tightening has been brutal to risky assets, everyone believes that as soon as the Fed is politically able, it will turn the taps back on. If you don’t believe that, then you believe central banks will allow debt-backed assets to deflate. Every single central bank was created to fight this exact outcome, and we can therefore be confident that this time is no different. The only real unknown — and it’s the same unknown every cycle — is timing.

As I argued in the first part of this essay, the realities of the Ukraine war dictate that America must respond with more dollars to help its allies afford to continue eschewing cheap Russian food and fuel. If there wasn’t an ongoing war with America’s perennial ideological rival, then the timing would be driven largely by the political winds in Washington. Cold weather, and Russia pushing its energy advantage over Europe — and to a lesser extent Japan — forces the Treasury and the Fed to act now. Obviously, these institutions would rather enhance the ruling party’s inflation-fighting credentials by continuing to reduce the quantity and raise the price of money into November, but they won’t be left with much of a choice. Winter does not bend to the political machinations of the Empire.

The US may be able to support their allies by printing money and buying their bonds while also claiming to be continuing QT, but it would be the accounting equivalent of sleight of hand magic — and the reality is that the money faucet would be flipped back on.

“Ok Arthur, I love your writing, but wen bottom?”

Some of you savvy readers might have bottom ticked the market by buying Bitcoin below $18,000. That level will probably constitute the bottom; however, a bottom is usually tested again before the bull market begins in earnest. Bear market rallies are viscous in their ability to force short covering. I don’t believe this rally from $18,000 to almost $24,000 is any different.

The market will definitely bottom before a change of US Treasury or Fed policy is announced. But, however sound my arguments may be, I have no idea what the timing of such an announcement will be. That is why, for my portfolio at least, it pays to wait. I am in no rush to sell fiat and increase the weighting of crypto in my overall portfolio. I will wait for a declarative statement from one of these two government agencies that supports my hypothesis.

I obviously sacrifice the ability to bottom tick the market by waiting for these assurances. But I believe the worst outcome, for someone investing on a six month or longer time horizon, is getting shook out of your position due to market volatility and a wavering commitment to the position. The market chop will obliterate anyone without proper belief in their investment thesis.

If you buy my hypothesis, then expect the quantity of dollars supplied outside of the US to increase as the Fed buys Japanese and EU bonds. When this policy is announced, investors should consider going long and strong crypto. If you fancy yourself a TRADER, then you can set tight downside stops and venture into the crypto maelstrom early to catch better bargains.

If it comes to pass that I got it all wrong, then my base case is that the Fed pivots by the second quarter of 2023. The election will be over, and the US and global economy will be in shambles. The Fed can then get back to its mission of pumping asset prices and reviving the wealth effect for its wealthiest citizens. That was their plan all along, but every two years, they have to pretend to care about plebes.

A quick thought experiment before we return to the inn: recorded inflation metrics around the developed world are at all-time highs. If these central bankers really cared about fighting inflation, they would immediately raise the short-term rates to match inflation levels. Imagine if the Fed raised rates to 9%, which is about the level of the latest CPI print. It likely would stop many components of inflation in their tracks, albeit at the expense of the ruling class (aka asset holders). If the Fed is really prepared to do the unspeakable to fight inflation, then they should do it already! Otherwise, this inflation-inspired Kabuki theatre is getting quite boring.

Those fools do not know whose table they have graced. Thankfully, my disguise fooled these knaves, and I kept my disgust for their quest well-hidden.

Lady Lagarde returned to her quarters, and I sat awake in the moonlight. Out of the corner of my eye, I saw bubbles gently rising to the surface of the pond at the front of the inn. I knew it was time.

Dear reader, this pond is no ordinary body of water. It is truthfully more lake than pond. Neither its depths nor its contents are known to most humans. But you do not know my true provenance. I have a very special friend who resides in the lake, and from time to time, this beautiful creature graces me with her presence.

Slowly, the most graceful and elegant hand emerged from the pond. Draped in simple gems that glittered under the moonlight, this hand clutched a flaming sword– one which I recognised instantly. She held Excalibur, a weapon forged from the life force of the one true god, Lord Satoshi. Only a true servant of the Lord could wield such a treasure.

Excalibur’s hilt called to me. I sprinted to the lake and grabbed my birthright from the guardian of the pond.

Excalibur’s flames shone so bright that it awoke my guests from their deep slumber. The three of them rose and ran out to meet me on the shore of the pond.

“You have deceived us!” Sir Powell shouted out to me. “You are not some simple innkeeper– you must be of noble blood yourself!”

“Silence!” I yelled back. “You are right — I am no innkeeper. And this is no ordinary rest stop on the Road to Hyperinflation.”

“What is that you hold in your hand, and why does it shine with such brilliance?” Lady Lagarde squeaked.

“M’lady, this is Excalibur. Behold its power! Excalibur was given to me so that I may slay those who might inflict hyperinflation upon this good Earth.”

With one swift motion — so quick that the synapses of the human brain could not register that I had moved — I swung Excalibur and carved a “B” on the chests of Sir Powell, Lady Lagarde, and Kuroda-dono.

“ARGGHHHH!” They writhed in pain. “What is this sorcery?!” Their flesh sizzled and curled like pieces of fatty bacon in a hot iron skillet.

“You shall forever know my name, and the name of my Lord. My name is King Arthur, my sword is Excalibur, and I serve the one true Lord, Satoshi. I have just carved “B” for Bitcoin onto your sinful bodies. Bitcoin is powered by your magic money printers, and it grows stronger the more you print. You should be cowering in fear — for Bitcoin is the tool of my Lord, and my Lord hath no mercy for the apostate.”

The trio continued to squirm, their skin still burning from Excalibur’s painful bite.

“DO YOU REPENT!?” I thundered with all my might.

. . .

Find out in the not so distant future what happens to Sir Powell, Lady Lagarde, and Kuroda-san. This story is not finished, and their penance is not complete.

In the meantime, King Arthur requires your service. Go forth with me on the righteous path to slay the dragon of hyperinflation unleashed by the followers of false gods.